Learn & Compare:

Mortgage Insurance Vs. Personal Insurance

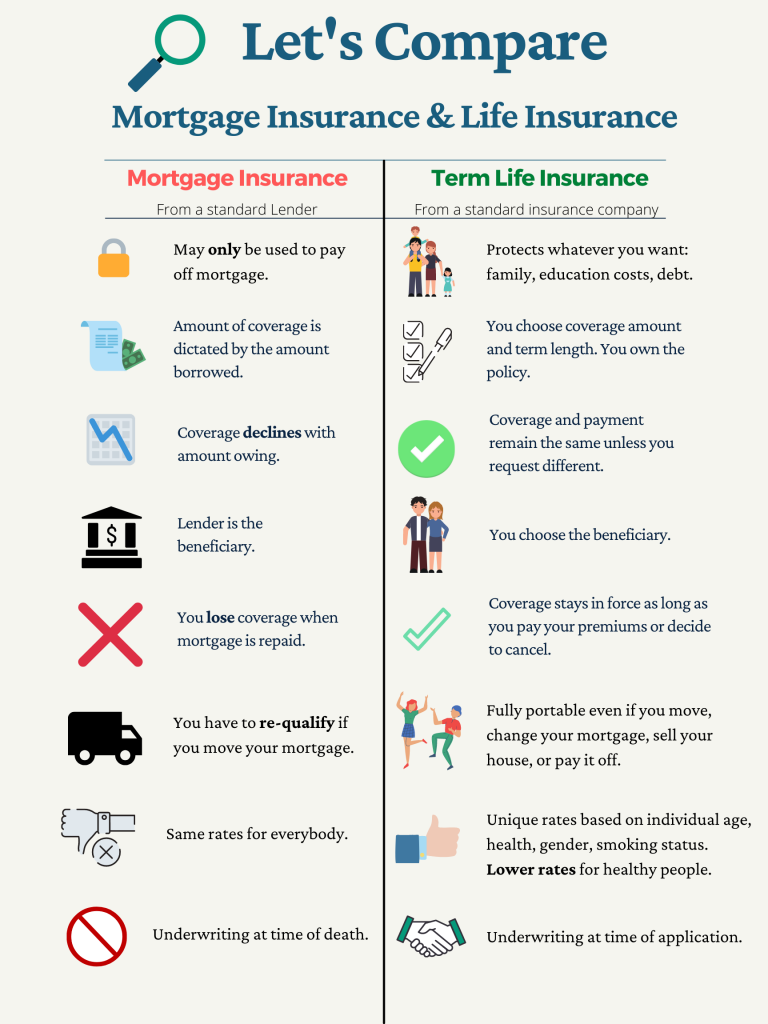

There are some key difference between mortgage insurance (creditor) and personal insurance. Mortgage (sometimes known as creditor insurance) is usually sold by banks, credit unions or sometimes a mortgage broker.

Personal insurance is typically offered through brokers, some financial advisors, and sometimes directly by insurance companies.

Mortgage insurance may only be used to pay off your mortgage if you pass away. Where as personal insurance can cover your mortgage as well as other things. Such as: protect your family, your children or future children’s education costs, as well as any other form of debt, future taxes owing or other estate needs.

With creditor insurance the lending institution is the only beneficiary of the policy, (the bank receives the funds if you pass away) and the amount of coverage is simply the amount owing on your loan/mortgage.

Conversion.. Personal insurance can typically be converted to other types of coverage. (think term converted into permanent coverage) whereas mortgage insurance can not.

With personal insurance you choose the coverage amount, term length, as well as one or multiple beneficiaries. This means your family or beneficiary can choose to partially pay down the mortgage if you pass away, or choose another purpose for the funds. It does not necessarily have to go towards the mortgage.

The amount of coverage is constantly declining with mortgage insurance (since the coverage amount is the mortgage owing) this means you are paying for coverage that is always declining every time you make a mortgage payment.

With personal insurance, the amount of coverage is level for the chosen term, and the premium (payment) amounts are locked in for that term length as well.

For example: You purchase a house for $300,000. You pass away a few years later when the amount owing on your mortgage is now $250,000. With mortgage insurance the $250,000 is now paid off. With personal insurance the full $300,000 is paid to your family.

If you pay off your mortgage or sell your house you will then lose the mortgage insurance. With personal insurance you can choose to keep the insurance for another purpose, or cancel it.

If you move or change your mortgage provider, you will likely have to re-apply/re-qualify for mortgage insurance and potentially be subject to increased rates due to age.

Personal insurance is not directly tied to your mortgage so is not affected if you refinance or move your mortgage, so there is no need to re-apply/re-qualify.

With mortgage insurance they use standard rate charts based on gender, age and smoking status so everyone gets the same rates.

Personal insurance can be applied for either as fully underwritten or non-medical, but rates are personalized to you and your current health. This means that most people (especially people in stable health) can qualify for lower rates and lock in those rates for 10, 20, 30 years etc.

Perhaps the most important difference.. Underwriting at time of death vs. time of application. “Underwriting” is the insurance provider deciding if they are going to give you insurance and at what rate and if there will be any exclusions.

Mortgage insurance is typically underwritten at time of claim (death) which means your claim could be denied for a pre-existing health condition, but your family won’t know until it’s too late.

Personal insurance the underwriting takes place at the time of application and sometimes medical information can be requested. If there is a health issue the rates could be changed.

That said, once a personal insurance policy is issued and the contract is in-force. The benefit amount must be paid upon death unless there was fraud.

So even if your rates were increased with personal insurance due to a major health condition, it is still preferable to know you are covered in the event of death. Rather than hope and pray your mortgage insurance policy pays out.

Isn’t certainty the whole point of insurance in the first place?